Blockspace enabled Ecosystem building

I remember reading a great piece in 2023 by 0xPerp, on blockspace being a “class of commodities” vs “a commodity” and it holds good even today.

Why? Not all blockspace is built the same, but they all have similar properties and are valued by some multiplier of economic activity (demand for blockspace), its quality, security, and the scarcity of blockspace.

The goal of a blockchain is to maximize economic activity, maximize quality of economic activity, and decentralization (+ security) to maximize token value. These are not the only factors that govern the value or a specific indication of how to value a chain, but it is a general indicator of how.

With applications now being more mature and require basic features like low latency, the differentiator now becomes positioning or targeting applications that cannot thrive on existing chains (because of a certain hierarchy).

Different blockchains have different definitions of what a “good block” looks like. This will happen irrespective of whether the team that builds the blockchain defines this or not.

In general purpose and neutral blockchains like Ethereum and Solana, the tokenholders decide who gets to order transactions or what transactions to prioritize. We’ve seen this happen with Ethereum (”are Rollups good for Ethereum?” “Who does MEV accrue to?”) and more recently with Solana on who has the power to order transactions. Apps or Validators? (Jito vs Harmonic). At some point, the incentives might not align with the vision with which the blockchain was built. Example: Right now stakers/validators on Solana don’t want to give up additional yield/revenue by opting into Jito. Jito claims that BAM will grow economic activity eventually as it encourages newer types of applications, but Harmonic says the pie will grow irrespective (Horizontal vs. Vertical growth of economic activity). All this happened even though Solana defined what economic activity growth was (Bring Nasdaq on chain -> trading activities).

Hyperliquid on the other hand was very intentional by designing their blockspace and defined what a “good block” looks like and what execution should look like. Hyperliquid prioritized cancellations over new orders, making market-making viable and shaping their entire ecosystem around deeper orderbook liquidity. Hyperliquid did not just attract orderbook apps; they made orderbook apps possible by design, and hence you don’t see random Aave or Uniswap forks popping up on HyperEVM. They defined what economic growth is on the chain. The success of HIP-3 DEXs is a testament to good blockspace design.

Tempo clearly prioritizes all stablecoin transfer transactions (contract/EOA) and hence positioned itself as the best layer to house all of global payments. They defined economic activity growth to be growth of payments on that chain.

MegaETH is interesting. Block production is so fast and transaction landing is so cheap that there is no scope of “fighting” for blockspace. By the time you click a button twice, the transaction from the second click probably gets included in the next block. This instantly reduces REV-maxxing, but does that mean MegaETH is not valuable? No.

Multiple variables, still no consensus on what matters

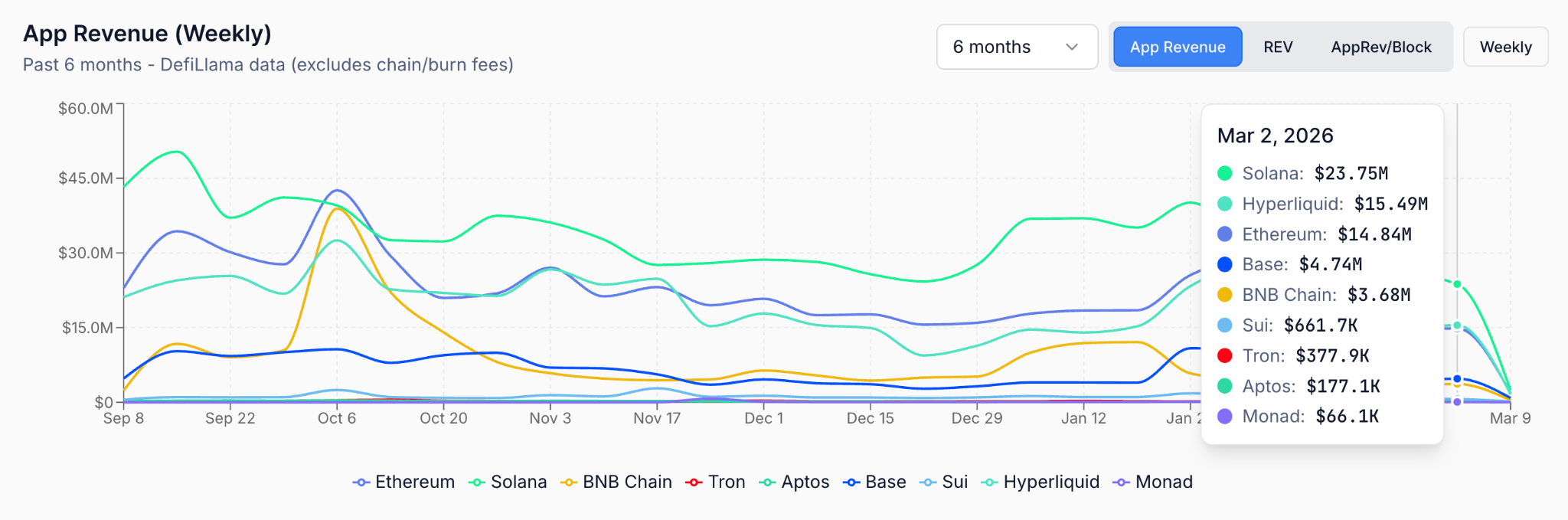

Look at app revenue over 6 months. Solana generates $1.5B annually. Ethereum generates $780M. Hyperliquid generates close to $1B - surpassing Ethereum’s total economic activity with 16 validators instead of 1 million. Trace the lines - Solana’s app revenue has been consistently at or above Ethereum since August, relatively stable between $25-35M/week, and is valued lower than Ethereum.

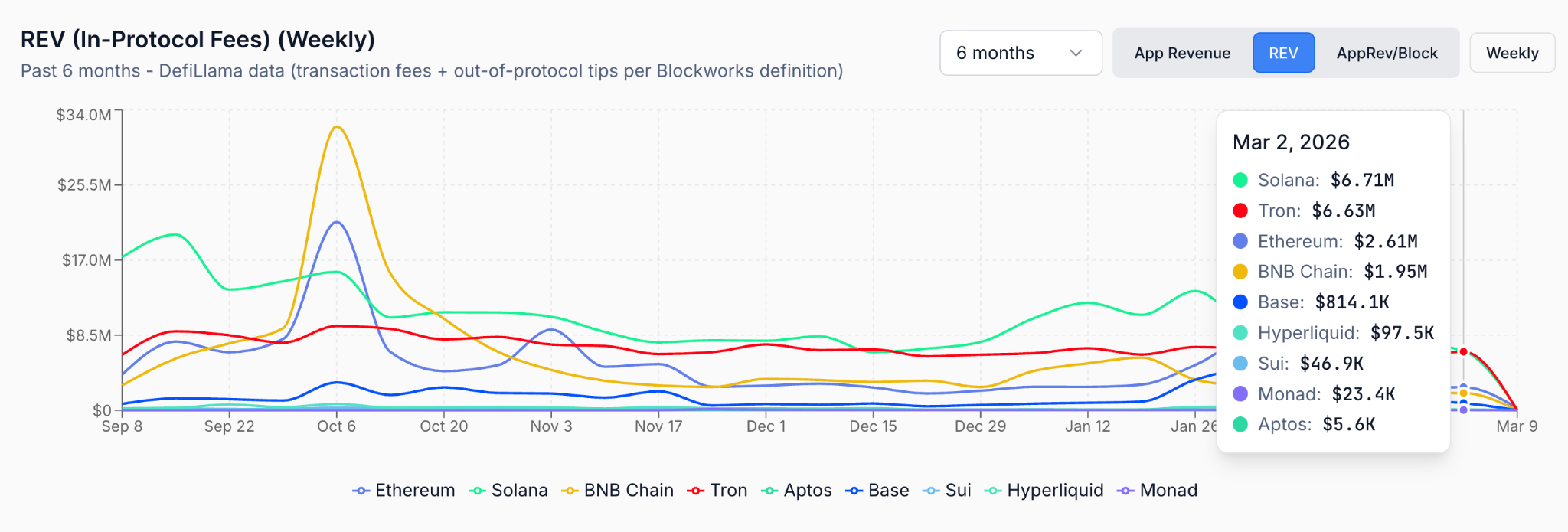

Now look at REV . Solana started at $25M/week in August and has declined to ~$10M/week over the past 6 months. Ethereum has been bouncing between $5-12M/week with no clear trend. Tron has been stable at $7-8M/week for the entire period. Yes again, there is a disparity in their valuations.

Here’s the disconnect: Solana’s app revenue stayed stable at $30M/week while REV halved from $25M to $10M. The economic activity didn’t disappear - validators are possibly just capturing less of it.

Same app revenue for Hyperliquid and Ethereum, but Hyperliquid validators capture 78% less in fees. This isn’t dysfunction - it’s intentional design. Hyperliquid needed high-frequency market makers to provide tight spreads and low friction for users, so they designed blockspace that doesn’t extract aggressively and prioritizes cancel orders for makers.

The L2 graveyard teaches the same lesson

Early L2s assumed that assets (and hence apps and users) would natively port from mainnet solely because mainnet was expensive and slow. This failed spectacularly. Asset issuers weighted decentralization + existing liquidity much higher than execution speed - this is the state/history problem that persists even today. Financial primitives care about security guarantees first, performance second.

Base doesn’t have high-quality RWAs, probably because of centralization risks. It would be interesting to see if Coinbase/ one of its portfolio products become an asset issuer themselves and expand that ecosystem. But again, Coinbase is the single point of failure.

Building infrastructure first, then experimenting with applications afterward will hit a ceiling unless something is forcibly put there. The market has matured too much to be forgiving of that backwards approach.

MegaETH is doing it right - they knew they wanted real-time consumer applications (and didnt bother with RWAs or called themselves the future of finance) with sub-millisecond latency requirements, then built purposeful infrastructure to support exactly that. Hyperliquid did the same for orderbook DEXs. The common denominator? Honesty and purpose about what an ideal block looks like, and being willing to sacrifice certain metrics (REV, validator count, whatever) to achieve the target ecosystem. They prioritized app revenue.

The future is about intentional trade-offs. Solana’s REV halved while app revenue stayed flat. Base made blockspace cheap and hasn’t found PMF with RWAs or high performance trading use cases. There are multiple variables at play - REV, app revenue, decentralization, validator profitability - and the market is still figuring out which combinations actually matter. To offset risk by placing all bets on app revenue, MegaETH also has its USDM stablecoin revenue that could be bucketed into “REV” for the MEGA token.

I think we will see some patterns emerging over the course of time, and I’ve made a dashboard to help track them all in one place:

https://blockspace-dashboard.replit.app/

DM me on X for any feedback